This successfully removes the ceiling on monetary risk for individuals in the individual exchanges. The subsidies for insurance premiums are offered to individuals who purchase a plan from an exchange and have a household earnings between 133% and 400% of the hardship line. Section 1401(36B) of PPACA discusses that each subsidy will be supplied as an advanceable, refundable tax credit and gives a formula for its computation: Except as supplied in stipulation (ii), the applicable percentage with respect to any taxpayer for any taxable year is equal to 2. 8 percent, increased by the number of portion points (not greater than 7) which bears the very same ratio to 7 portion points as the taxpayer's family income for the taxable year in excess of 100 percent of the hardship line for a household of the size included, bears to a quantity equal to 200 percent of the hardship line for a family of the size included.

A refundable tax credit is a method to provide government advantages to individuals who may have no tax liability (such as the made income tax credit). The formula was altered in the amendments (HR 4872) passed March 23, 2010, in section 1001. To qualify for the subsidy, the recipients can not be qualified for other acceptable coverage. The U.S. Department of Health and Human Services (HHS) and Internal Revenue Service (Internal Revenue Service) on May 23, 2012, issued joint last guidelines concerning implementation of the brand-new state-based health insurance coverage exchanges to cover how the exchanges will identify eligibility for uninsured people and employees of small companies seeking to buy insurance on the exchanges, as well as how the exchanges will manage eligibility determinations for low-income people looking for newly broadened Medicaid benefits. How does cobra insurance work.

3% $2,778 $8,366 $4,000 250% $55,125 8. 05% $4,438 $6,597 $1,930 300% $66,150 9. 5% $6,284 $4,628 $1,480 350% $77,175 9. 5% $7,332 $3,512 $1,480 400% $88,200 9. 5% $8,379 $2,395 $1,480 In 2014, the FPL is forecasted to equivalent about $11,800 for a bachelor and about $24,000 for a household of four. See Subsidy Calculator [] for specific dollar amount. DHHS and CBO estimate the average annual premium cost in 2014 would be $11,328 for a family of 4 without the reform. In the specific market, in some cases considered the "recurring market" of insurance coverage, [] insurance companies have actually usually used a process called underwriting to ensure that each individual spent for his/her actuarial worth or to reject coverage altogether.

The smart Trick of How Much Is Homeowners Insurance That Nobody is Discussing

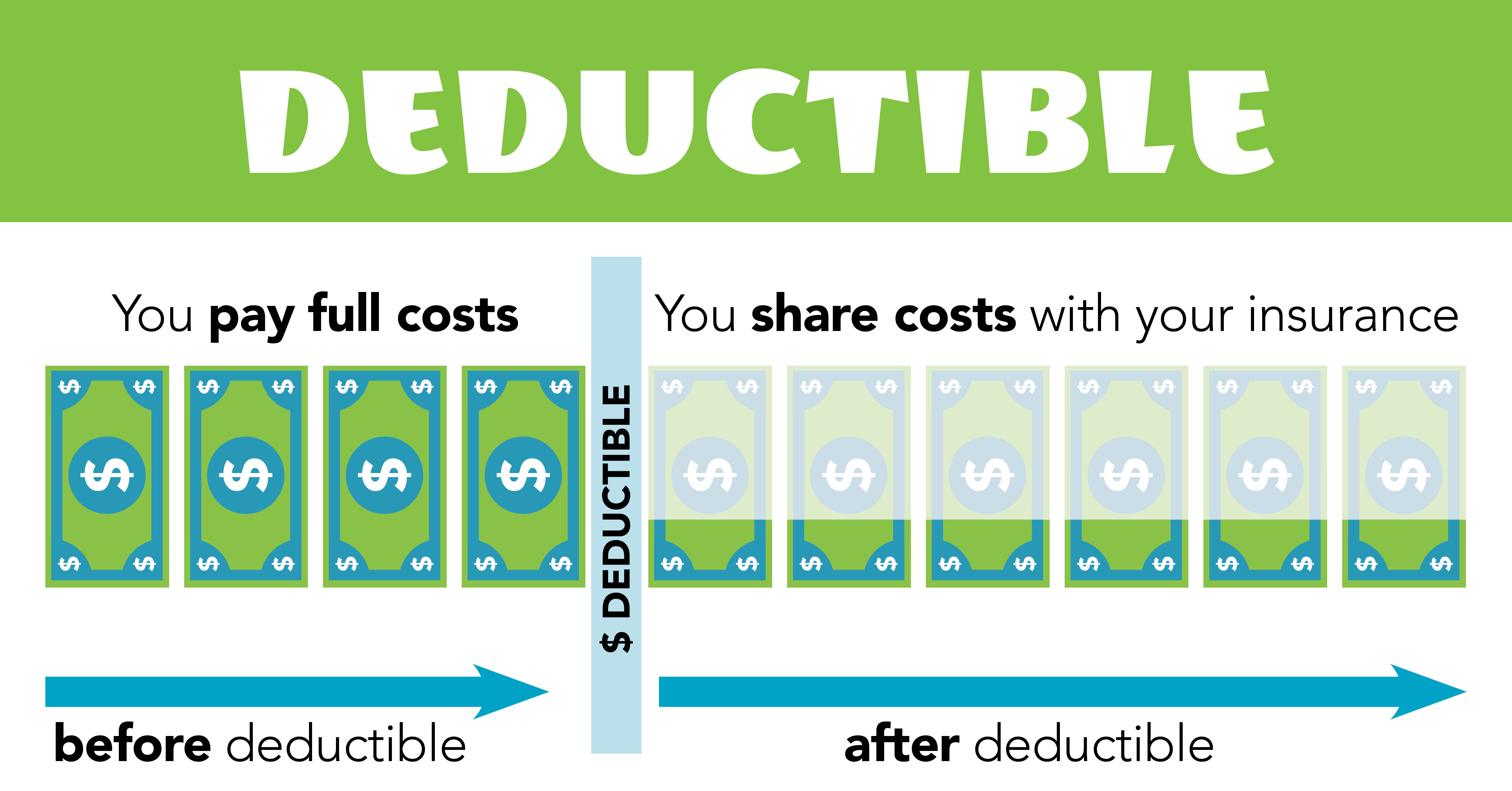

The very same memorandum said that 212,800 claims had actually been declined payment due to pre-existing conditions which insurance companies had service strategies to limit money paid based upon these pre-existing conditions. These individuals who may not have received insurance coverage under previous market practices are guaranteed insurance coverage under the ACA. Hence, the insurance exchanges will move a greater quantity of financial danger to the insurers, but will help to share the cost of that risk amongst a bigger swimming pool of insured individuals. The ACA's prohibition on rejecting protection for pre-existing conditions started on January 1, 2014. Previously, several state and federal programs, consisting of most just recently the ACA, offered funds for state-run high-risk pools for those with formerly existing conditions. The Medical Insurance Market is a platform that offers insurance plans to people, households, and small companies. The Affordable Care Act (ACA) established the Marketplace as a method to extend medical insurance coverage to countless uninsured Americans. Lots of states use their own marketplaces, while the federal government handles an exchange available to citizens of other states. The Medical Insurance Marketplace is an entrance for people, households, and small organizations to access health insurance coverage. It was created following the passage of the Affordable Care Act. The Marketplace is available to those who don't have access to medical insurance through employer-sponsored plans.

A variety of states have marketplaces and the federal government has an exchange available for citizens of the states that don't have their own. The Medical Insurance Market is a crucial element of the Affordable Care Act, a healthcare reform signed into law by President Barack Obama in 2010, likewise understood as Obamacare. The law instructed states to set up their own exchanges where people or families without employer-sponsored coverage might compare plans. Numerous states, nevertheless, have actually picked not to develop a marketplace and have signed up with the federal exchange. The Market helps with competition amongst personal insurance providers in a central location where individuals who do not have access to employer-sponsored insurance coverage can discover an ideal plan.

Typically, this duration happens in November and December of the year prior to the year in which the protection will take effect. Customers can request a special enrollment duration when it comes to a certifying occasion such as the birth http://sites.simbla.com/45e1a046-6bd8-c277-ae44-3d8219847965/saaseyywrb9956 of a kid, marriage or the loss of another insurance strategy. The Marketplace categorizes plans into 4 tiers: bronze, silver, gold, and platinum, in the order of least to greatest protection. The greatest tier, platinum, includes plans that cover around 90% of health costs, but is likewise the most pricey. Lower-income individuals and households can receive additional savings on all the medical insurance plans offered on the exchange through premium tax credits and cost-sharing reductions.